As of June 10th, most mortgage rates are showing a slight dip compared to yesterday, with the notable exception of the 15-year fixed loan, which has nudged upwards. This means there might be a small window of opportunity for some buyers, but the overall picture remains one of cautious movement rather than a dramatic shift.

It feels like just yesterday we were talking about rates heading into the low 6s, and now, here we are, back to watching the numbers closely. As someone who's been following the housing market for a good while now, I know how much even small fluctuations can mean for your budget. So, let's dive into what's happening with today's mortgage rates and what it could mean for you.

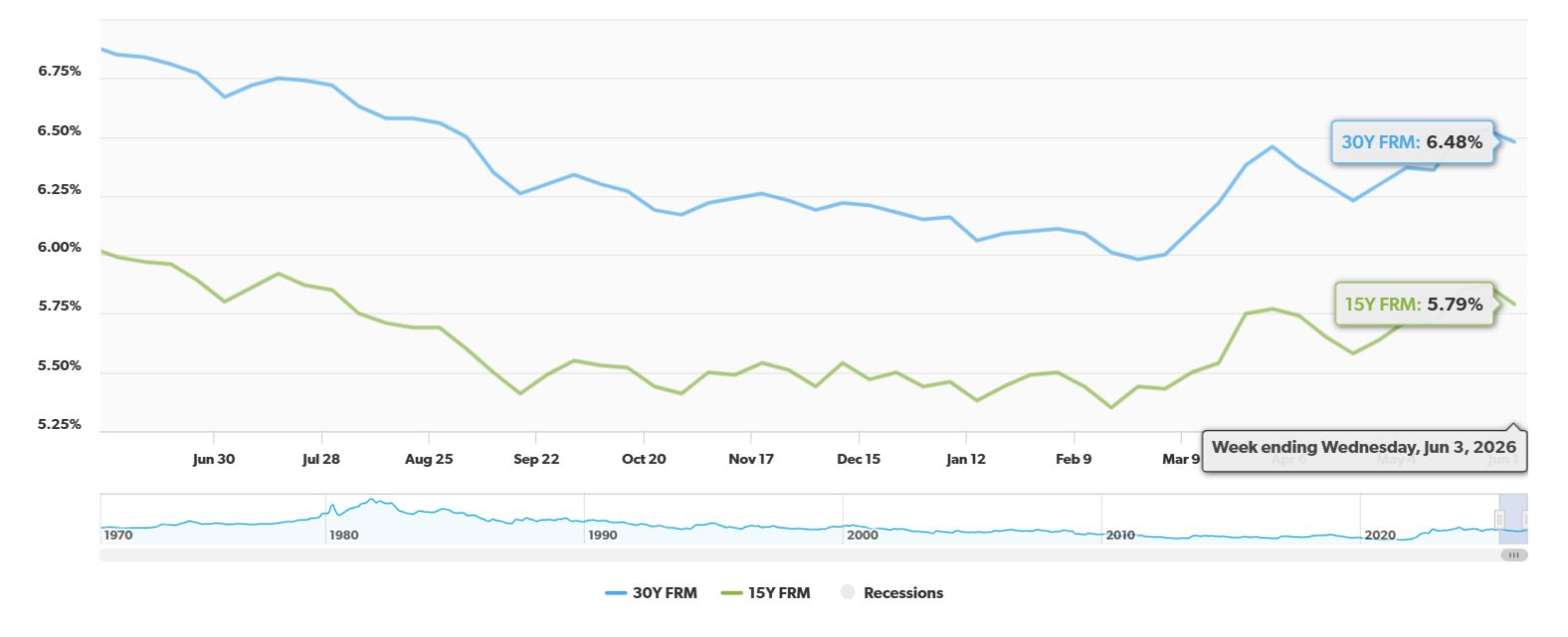

Today's Mortgage Rates, June 10: Buyer Costs Ease Slightly as 30‑Year Fixed Drops to 6.33%

What the Numbers Say Today

The most recent data gives us a snapshot of where things stand on June 10, 2026. It's important to remember these are national averages, and your specific rate will depend on your credit score, down payment, and the lender you choose.

Here's a breakdown of what Zillow is reporting for purchase loans:

| Loan Type | Rate Today (June 10) | Change from Yesterday |

|---|---|---|

| 30-year fixed | 6.33% | Down 8 basis points |

| 20-year fixed | 6.26% | Down 14 basis points |

| 15-year fixed | 5.89% | Up 8 basis points |

| 5/1 ARM | 6.26% | Down 14 basis points |

It’s interesting to see the 30-year and 20-year fixed rates moving down, while the 15-year is inching up. This suggests a bit of a mixed bag. The 5/1 ARM is also showing a nice dip, which could be attractive for those looking for a lower initial payment.

For those who have served our country, VA loans also have their own set of rates:

| Loan Type | Rate Today (June 10) |

|---|---|

| 30-year VA | 5.80% |

| 15-year VA | 5.50% |

| 5/1 VA | 5.69% |

Why Are Rates Moving Like This?

It’s easy to get caught up in just the numbers, but understanding why they move is crucial. Honestly, the mortgage rate environment right now feels a bit like being on a rollercoaster that’s mostly stuck on a middle track – it's volatile and seems determined to stay within a certain range. We’re seeing rates hovering between 6.0% and 6.7%, not really breaking free.

A big player in this is the ongoing geopolitical situation. Remember earlier this year when rates flirted with dipping below 6.0%? Well, events in places like the Middle East, specifically involving Iran and the Strait of Hormuz, have caused oil prices to spike. This, in turn, has made it harder for inflation to cool down. We’re looking at a US consumer price index (CPI) that’s stubbornly around 3.8%.

On top of that, the Federal Reserve, under its new Chair Kevin Warsh, has made it clear they're not rushing to cut interest rates. The job market is still showing strength, with reports like the 172,000 jobs added in May. This resilience means the Fed is less pressured to stimulate the economy with lower borrowing costs. In fact, some economists are even whispering about the possibility of a rate hike if inflation doesn’t start cooperating. So, any hope of a quick return to those ultra-low rates we saw during the pandemic (think 3% to 4%) is pretty much off the table for the foreseeable future. Housing authorities like Fannie Mae and the Mortgage Bankers Association are adjusting their predictions, suggesting that 30-year fixed rates will likely average between 6.3% and 6.5% for the rest of the year.

What This Means for You: Smart Moves to Make

So, what can you do with this information? It’s all about being strategic.

1. Rethink Your Refinance Plan

- The Action Plan: If you’re thinking about refinancing, my advice is to only seriously consider it if your current mortgage rate is above 7.125%.

- The Logic: Moving from a 7.5% rate down to today’s 6.33% would obviously save you money each month. However, if your current rate is already below 6.5%, the closing costs associated with refinancing will likely eat up any savings you’d see. It just doesn't make financial sense in that scenario.

2. Master the Rate Lock Game

- The Action Plan: If you’re currently under contract to buy a home, be ready to lock in your rate the moment you see a short-term dip in the market.

- The Logic: Mortgage rates are sensitive to sudden jumps in things like the 10-year Treasury yields and those unpredictable energy markets. If you’re waiting for a rate below 6.0%, you could miss your chance if geopolitical news causes rates to spike again. Acting quickly when you see a favorable movement is key.

3. Consider Shorter Terms or Different Loan Types

- The Action Plan: Take a close look at how a 15-year fixed loan or a 7/1 Adjustable-Rate Mortgage (ARM) would fit your budget.

- The Logic: A 15-year fixed loan, while it comes with a higher monthly payment, will save you a significant amount of money in interest over the life of the loan – often more than half of what you’d pay on a 30-year. A 7/1 ARM, on the other hand, offers a lower initial rate for the first seven years. This can provide some breathing room financially while you wait for the broader economic picture to stabilize. It's a trade-off, but a potentially worthwhile one for some.

4. Get Creative with Your Closing Costs

- The Action Plan: Explore options like negotiating a temporary seller buydown (2-1 or 3-1) or paying for discount points upfront.

- The Logic: In today’s market, asking the seller to help with a temporary buydown can lower your interest rate by 2% in the first year and 1% in the second year. This can significantly reduce your immediate housing costs, giving you more time to plan for a permanent refinance down the road if rates become more favorable. Paying discount points out-of-pocket is another way to permanently lower your rate, but you need to do the math to ensure it makes sense for how long you plan to stay in the home.

Navigating today's mortgage market requires a good understanding of the numbers and the forces behind them. By staying informed and being proactive, you can make the best decisions for your homeownership journey.

VS

Out‑of‑State investors can compare Indiana’s affordable rental with higher cap rate vs Florida’s newer A+ property with stability. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain high in 2026, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- Mortgage Rates Predictions Backed by 7 Leading Experts: 2025–2026

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?