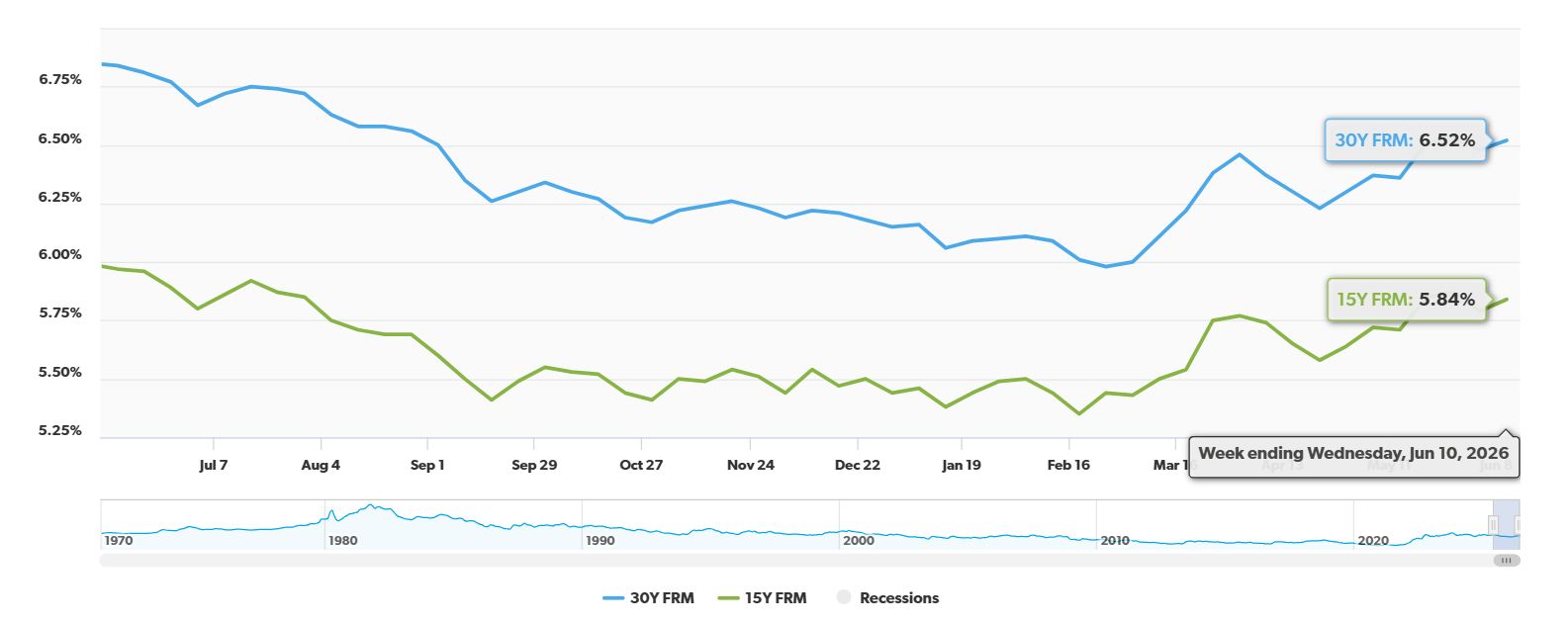

If you're thinking about buying a home or refinancing your mortgage, you've probably been watching mortgage rates closely. As of June 17, the rates have seen a small dip, with the popular 30-year fixed mortgage rate now at 6.26%. While this is a tiny bit lower than yesterday, it's still a bit higher than what we saw earlier this year.

Today's Mortgage Rates, June 17: Rates Edge Down But Market Still Tight

It feels like just yesterday we were seeing rates closer to 6.0%, and now we're hovering a bit above that. Why is this happening? Well, a few big things are going on in the world that are making these rates stick around. Think of it like a big puzzle where different pieces affect how much you pay for your home loan.

What's Happening with Today's Mortgage Rates?

Let's break down what the numbers are telling us today. According to Zillow, here's a snapshot of what mortgage rates look like on June 17:

| Loan Type | Interest Rate |

|---|---|

| 30-year fixed | 6.26% |

| 20-year fixed | 6.06% |

| 15-year fixed | 5.73% |

| 5/1 ARM | 6.30% |

| 7/1 ARM | 6.03% |

| 30-year VA | 5.80% |

| 15-year VA | 5.38% |

| 5/1 VA | 5.58% |

As you can see, most of the rates have nudged down just a tiny bit. The 30-year fixed rate, which is what most people choose for their homes, dropped by 5 “basis points” (that's just a fancy word for a small change in percentage) to land at 6.26%. The 15-year fixed and the 5/1 ARM also saw a small dip of 1 basis point.

Why Aren't Rates Much Lower? The Big Picture

Even though we saw a small drop, rates are still higher than they were at the start of the year. This is mainly because of a few big factors that are like strong winds pushing against lower rates. I’ve been watching this market for a while, and it's clear that these issues aren't going away overnight.

Here are the main things making rates stick around the current levels:

- Trouble Far Away, Trouble Here: There's a military conflict happening in Iran. This is really important because Iran is a big supplier of oil. When there's worry about oil, prices go up. Since oil is used for almost everything – like shipping goods and making things – higher oil prices make everything else cost more. This is called inflation. Even though there have been some small agreements to help ships get through safely, the worries about prices going up for a long time are still there.

- Prices Keep Going Up: You know how sometimes the price of your favorite snack goes up? Well, that's happening with lots of things for everyone. The government wants prices to only go up about 2% each year. But right now, prices are going up much faster, around 4.2%! When prices go up quickly, the money people have saved doesn't buy as much. To make sure they don't lose money because of this, banks and lenders have to charge more for loans, which means higher mortgage rates.

- Government Borrowing and Bonds: You might have heard about the government borrowing money. When the government needs a lot of money, it sells something called “bonds.” Think of bonds like an IOU from the government. When lots of bonds are being sold, the government has to offer a higher “interest rate” on these bonds to get people to buy them. Mortgage rates tend to follow what happens with these long-term government bonds, specifically the 10-year Treasury yield, which has been around 4.5%. So, the more the government borrows, the higher interest rates tend to go.

- The Federal Reserve's Tough Choices: The Federal Reserve (often called the “Fed”) is like the main banker for the country. They can help control how much money is out there and how much it costs to borrow. They actually lowered interest rates a lot late last year to help people. But now, with prices going up so much and people still having jobs, the Fed is rethinking things. They're not planning to lower rates anytime soon. In fact, some people are even starting to think they might have to raise interest rates to fight inflation, which would push mortgage rates even higher.

What Does This Mean for You?

When mortgage rates are a bit higher, it means buying a home can be more expensive each month. For example, if you borrow $300,000, even a small increase in the interest rate can add up to hundreds of dollars more on your monthly payment over the years.

- For Buyers: If you're looking to buy, it’s a good time to shop around for the best rate from different lenders. Also, try to save up a larger down payment if you can. A bigger down payment means you borrow less money, which can lower your monthly payments.

- For Refinancers: If you already have a mortgage, it might not be the best time to refinance if your current rate is lower than today's rates. However, if you need to lower your monthly payments for other reasons, it's still worth looking into options.

My Thoughts on Today's Rates

From where I stand, these rates are a bit of a balancing act. The world is dealing with some big challenges, from faraway conflicts affecting oil prices to how we manage our own country's money. The Federal Reserve is in a tough spot, trying to keep prices from going up too fast without hurting the economy too much.

For the average person, it means we need to be smart about our homebuying decisions. It's not just about the sticker price of a house; it's about the total cost over time, and that's heavily influenced by the mortgage rate you get.

I’ve seen rates go up and down over the years, and what’s happening now is a reminder that things don't always move in a straight line. The good news is that even with these rates, owning a home is still possible for many. It just requires a bit more careful planning and understanding of what's driving the numbers.

So, while today's mortgage rates might not be the lowest we've seen, they are what they are for now. Keep an eye on the news, talk to lenders, and make the best decision for your situation!

VS

Out‑of‑State investors can compare Tennessee’s newer rental with higher NOI vs Florida’s A+ property with strong yield. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain high in 2026, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- Mortgage Rates Predictions Backed by 7 Leading Experts: 2025–2026

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?