Imagine finally finding that perfect house, picturing your life there, only to realize the monthly payments are just out of reach. It’s a story many potential homebuyers know all too well these days. But what if things could change? Well, it turns out that even a seemingly small shift, like a 1% drop in mortgage rates, could make a huge difference, potentially opening the door for millions of people to buy a home.

Yes, according to research from the National Association of REALTORS® (NAR), a 1% decrease in mortgage rates could add about 5.5 million households to the pool of potential buyers, including 1.6 million renters who might finally be able to make the leap into homeownership. This is exciting news for anyone feeling priced out of the market right now.

How a 1% Drop in Mortgage Rates Could Unlock 5.5 Million Buyers

Why All the Fuss About Mortgage Rates?

You’ve probably heard a lot about mortgage rates lately. They've been a major topic because they directly impact how much house you can afford. Think of it like this: the mortgage rate is the price you pay to borrow the money needed to buy your home. When that price goes up, your monthly payments go up significantly.

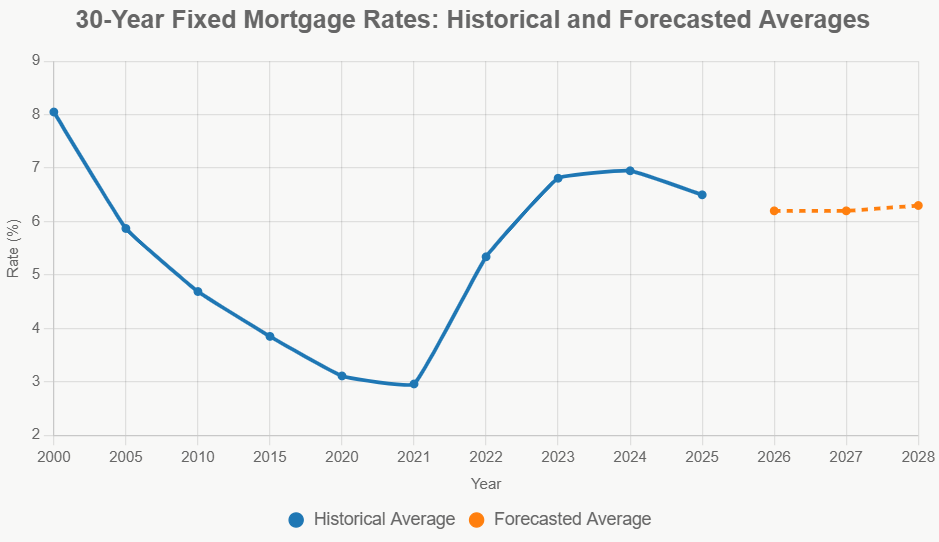

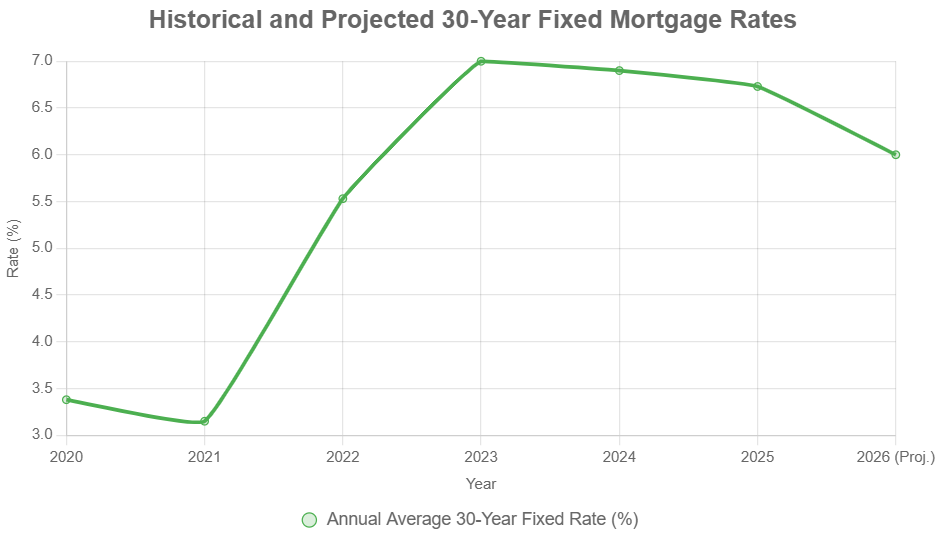

For a while now, we've been dealing with a double whammy: home prices shot up, and then mortgage rates followed suit. The National Association of REALTORS® pointed out that between mid-2022 and the end of 2023, average rates jumped from around 3% to over 7%. What does that mean in real dollars? For many people, it meant their monthly mortgage payment jumped by more than $1,000 compared to what they might have paid before the pandemic. Ouch.

From my perspective, this surge in costs effectively put many potential buyers on pause. They were ready and willing, but the numbers just didn't work anymore. It created what experts call an affordability crunch, freezing many buyers in their tracks.

Breaking Down the Numbers: What's a 1% Drop Worth?

Okay, let's talk specifics. How much difference does that 1% really make? It’s more than you might think.

Let’s look at an example cited by Matt Schulz, LendingTree’s chief consumer finance analyst. Suppose you're buying a $500,000 home and manage a 10% down payment ($50,000), leaving you needing a $450,000 mortgage.

- At a 7% interest rate: Your estimated monthly payment for principal and interest would be around $3,895.

- If rates dropped to 6.25%: That same loan would mean a monthly payment of about $3,672.

That's a saving of $223 per month. Now, imagine if rates dropped even further, say, to 6%. Based on calculations, the principal and interest payment on that same $450,000 loan could fall closer to $2,700 per month. That’s a potential saving of nearly $1,200 per month compared to the 7% rate!

While the ultra-low rates of 2020-2021 are likely behind us, a drop of 1% from current levels is a pretty big deal. NAR's research highlights that this kind of change could make homeownership achievable for millions more households. They estimate that 5.5 million households could be added to the potential buyer pool. Out of that group, a significant portion – 1.6 million – are renters who might finally see a path to owning their own place.

My take on this? It’s not just about saving a few bucks. It's about shifting the dream of homeownership from “maybe someday” to “maybe next year.” It changes the whole affordability equation for a massive number of people.

Who Gets the Biggest Boost?

When mortgage rates decrease, certain groups benefit more than others:

- First-Time Home Buyers: This group often has less equity built up and may be stretching their budget to afford a home. They are often the most sensitive to monthly payment changes. Rising rents have made saving for a down payment even harder, so a lower rate that reduces the monthly mortgage payment can be the key factor in making a purchase possible.

- Current Homeowners Looking to Move: Many homeowners refinanced or bought homes when rates were historically low. They might be hesitant to sell now because moving would mean taking out a new, much higher-rate mortgage. However, if rates drop significantly (like by 1%), it could lessen the “lock-in effect.” This might encourage them to sell their current homes, which in turn adds more properties to the market – increasing housing inventory for everyone. NAR economist Nadia Evangelou notes that lower rates help “both first-time buyers and current homeowners take the next step.”

It seems like a potential drop in rates could be a catalyst for activity across the board, helping people move up, move down, or buy for the very first time.

Are People Already Responding to Lower Rates?

It’s not just theoretical. Real estate professionals are already seeing signs that buyers are sensitive to rate changes.

Brad O’Connor, chief economist at Florida REALTORS®, shared during a recent NAR event that Florida saw a roughly 10% year-over-year increase in home sales this past fall. This uptick happened right when mortgage rates were starting to come down, hovering around 6.25%. Pending home sales in Florida were even up by 23% in October compared to the previous year. “We’re encouraged by how we see people are responding to lower interest rates already,” O’Connor mentioned.

Similarly, Ryan Price, chief economist at Virginia REALTORS®, noted a similar trend in his state. He observed an increase in sales in the fall that coincided with improved mortgage rates in September. He called these “early glimmers of hope” for what might come next year.

Personally, I’ve been hearing similar stories from agents and buyers in my area. When there’s even a hint of better affordability, the phones start ringing, and showings pick up. It really shows that pent-up demand is just waiting for the right conditions.

What’s the Crystal Ball Saying About Mortgage Rates?

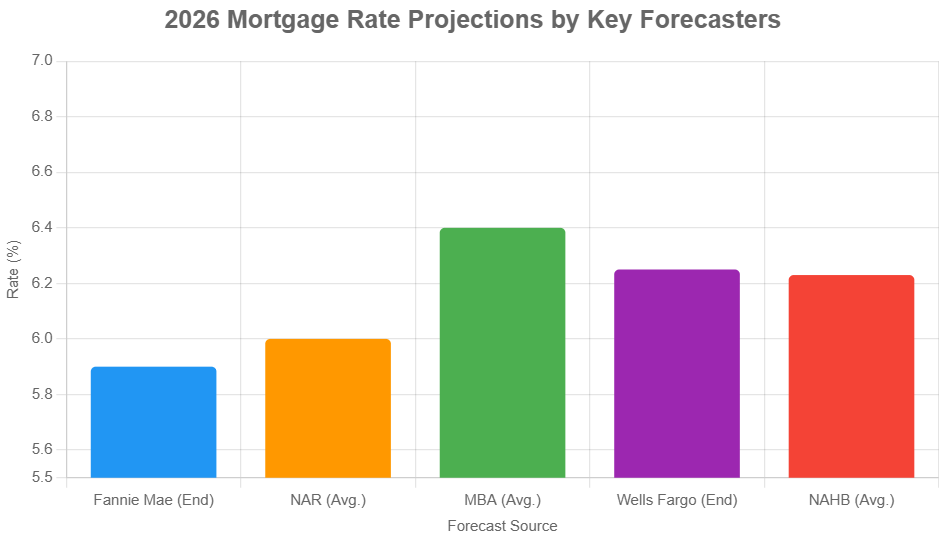

So, will rates actually drop significantly? The National Association of REALTORS® has a forecast suggesting that mortgage rates could fall to around 6% in 2026.

This prediction takes into account several economic factors, including:

- Potential cuts to the Federal Reserve's short-term interest rates.

- Ongoing trends in inflation.

- Government spending and national debt levels.

- Global trade impacts (like tariffs).

- The Federal Reserve’s management of its balance sheet (quantitative tightening).

- The performance of the 10-year Treasury yield, which is a key indicator for mortgage rates.

While predicting the future is tricky, this forecast offers a hopeful outlook for potential homebuyers.

Deep Dive: How a 1% Drop in Mortgage Rates Could Unlock 5.5 Million Buyers in Your Area

NAR’s analysis digs deeper, looking at how specific metro areas could be impacted if rates were to drop from, say, 7% down to 6%. It's not just about the national numbers; the effect can be felt differently from place to place.

Generally, a rate decrease means more households can afford the monthly payments associated with the median-priced home in that area. Here are some of the areas predicted to see the biggest jump in qualifying households from a 1% rate drop:

- Kalamazoo-Portage, Mich.: Potential for an 8% increase in households qualifying to buy.

- Yuma, Ariz.: 7.5% increase.

- Racine, Wis.: 7.5% increase.

- Hilton Head Island-Bluffton, S.C.: 7.4% increase.

- Rochester, Minn.: 7.4% increase.

Let's look at some specific examples provided by NAR to see the potential impact:

New York-Newark-Jersey City, NY-NJ-PA

- A 1% drop (from 7% to 6%) could increase the share of households qualifying to buy by 3.8%.

- This means roughly 285,972 more households could afford the median-priced home.

- If just 10% of these newly qualified households buy, that could lead to approximately 28,597 additional home sales in the next year or two.

Atlanta-Sandy Springs-Alpharetta, GA

- A 1% rate drop could boost the number of qualifying households by 5.4%.

- An estimated 126,038 more households would gain affordability.

- This could translate to about 12,604 additional home sales.

Dallas-Fort Worth-Arlington, TX

- This area might see a 4.9% increase in qualifying households with a 1% rate drop.

- Around 144,734 more households could afford the median home.

- An estimated 14,473 additional sales could result.

Los Angeles-Long Beach-Anaheim, CA

- Here, a 1% drop could mean 2.7% more households qualifying.

- That's about 122,864 additional households affording the median home.

- Projected additional sales could be around 12,286.

San Jose-Sunnyvale-Santa Clara, CA

- A similar rate drop could add 2.9% to the qualifying household share.

- This translates to about 19,835 more households qualifying.

- Potentially leading to 1,984 additional home sales.

(Note: These figures are based on NAR's analysis and projections. Actual impacts can vary.)

These examples illustrate the significant ripple effect lower rates can have, not just on individual buyers but on the overall market activity in major metropolitan areas.

My Thoughts: A Welcome Shift for Homeownership

As someone who follows the housing market closely, the potential impact of a 1% drop in mortgage rates is genuinely significant. While 6% is still higher than the rock-bottom rates we saw a few years ago, it represents a substantial improvement in affordability compared to the 7%+ rates.

This research from NAR gives me confidence that the market is dynamic. It shows that when affordability improves, people respond. Bringing 5.5 million potential buyers back into consideration could lead to a more balanced market, provide much-needed opportunities for aspiring homeowners, and help existing owners make their next move. It’s a crucial step towards making the dream of homeownership accessible again for a much larger slice of the population. If rates continue on the predicted downward trend, 2026 could indeed be a pivotal year for the housing market.

VS

Tennessee’s balanced rental vs Texas’s larger home with lower cap rate. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Talk to a Norada investment counselor (No Obligation):

(800) 611-3060

Also Read:

- Mortgage Rates Predictions Backed by 7 Leading Experts: 2025–2026

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?