This is the news many of us have been waiting for: the average 30-year fixed-rate mortgage has dropped by a significant 67 basis points, bringing it down to 6.18%. This welcome dip offers a timely boost for anyone dreaming of homeownership or looking to save money by refinancing their current home loan.

As the year draws to a close, it feels like the housing market is finally taking a collective deep breath. I've been following mortgage rate trends for years, and seeing rates ease like this, especially heading into the holidays, is always a positive sign. It’s not just a small fluctuation; this is a substantial drop from where we were just a year ago, and it can make a real difference in people's finances.

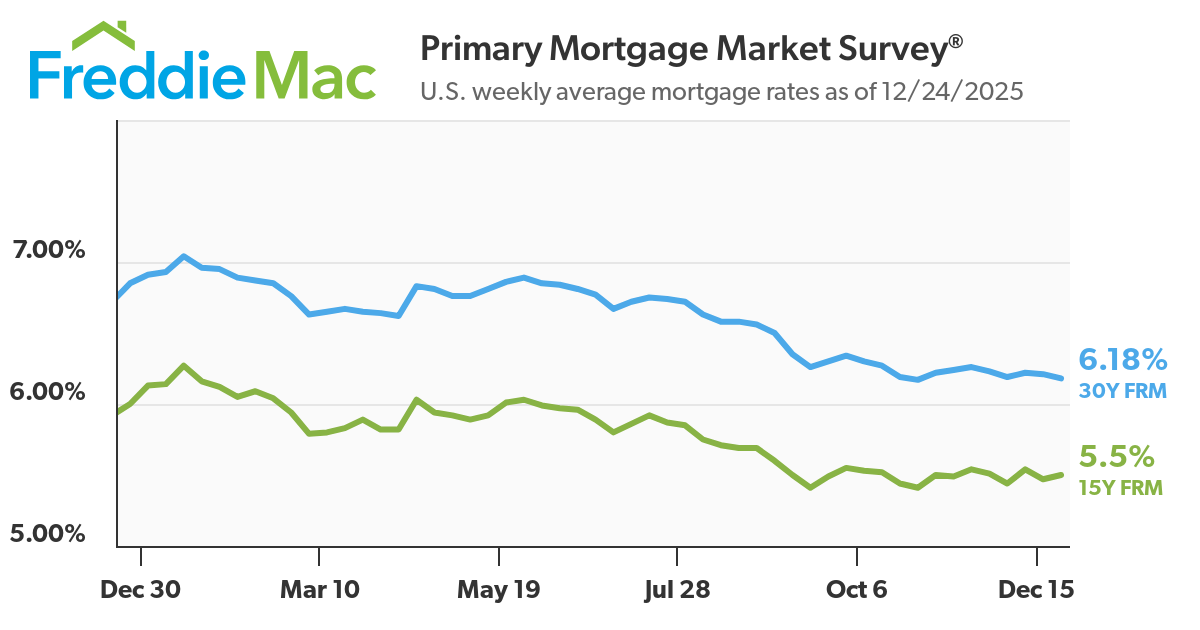

30-Year Fixed Rate Mortgage Drops Sharply by 67 Basis Points

What Did Freddie Mac Say? A Closer Look at the Numbers

Freddie Mac, a key player in the housing finance system, released its latest Primary Mortgage Market Survey®, and the numbers are worth celebrating. They track average rates across the country, and their findings paint a clearer picture of where we stand.

Let's break down the key figures from their survey as of December 24, 2025:

| Mortgage Type | Average Rate (Dec 24, 2025) | 1-Week Change | 1-Year Change |

|---|---|---|---|

| 30-Year Fixed Rate | 6.18% | –0.03% | –0.67% |

| 15-Year Fixed Rate | 5.50% | +0.03% | –0.50% |

As you can see, the 30-year fixed-rate mortgage is what really grabbed my attention this week. It's now sitting at 6.18%, which is incredibly close to its 52-week low of 6.17%. To put that into perspective, last year around this time, the average rate was a much higher 6.85%. That’s a difference of 67 basis points, and believe me, that adds up!

The 15-year fixed-rate mortgage also saw some movement, ticking up slightly to 5.50% this week. While it's not dropping as dramatically as the 30-year, it's still significantly lower than its 52-week high and has decreased by half a percentage point over the last year. This might make it a more appealing option for those who can handle a higher monthly payment in exchange for paying off their loan sooner.

Why This Drop Matters: Real Savings for Real People

So, what does a 67 basis point drop actually mean for your wallet? It’s more than just a number; it translates into tangible savings, whether you're buying a new home or refinancing your current one.

Let’s imagine you’re taking out a $300,000 loan secured by a 30-year fixed-rate mortgage.

- If you had locked in a rate at the year's high of 7.04% earlier in 2025: Your monthly principal and interest payment would be around $2,005.

- Now, with the current rate of 6.18%: Your monthly principal and interest payment drops to approximately $1,836.

That’s a saving of about $169 per month!

Think about that:

- That’s roughly $2,028 saved per year.

- Over the full 30 years of the loan, you could save over $60,000 in interest!

This kind of saving is a game-changer. It can free up money for other important things, like renovations, savings, or simply enjoying life a little more. From my experience, even a fraction of a percent difference in mortgage rates can have a monumental impact over the life of a loan.

Who Benefits Most from These Lower Rates?

1. Aspiring Homebuyers: For those looking to buy their first home or move to a new one, these lower rates can significantly improve affordability. They might be able to qualify for a larger loan than they initially thought, or perhaps afford a home in a more desirable neighborhood. It also provides more stability and predictability in budgeting, which is crucial when making such a major financial decision. I’ve seen buyers hesitate when rates are high, and then jump at the chance when they see them trending down. This is that chance.

2. Refinancers: If you already own a home and have a mortgage with a rate higher than 6.18%, now could be an excellent time to explore refinancing. Locking in a lower rate can reduce your monthly payments or allow you to pay down your principal faster. It’s like getting a financial do-over, and when rates are this low, it's an opportunity that shouldn't be missed. My advice to clients is always to run the numbers carefully, but if the savings are substantial, refinancing is often a smart move.

3. Those with Adjustable-Rate Mortgages (ARMs): While this specific piece of news is about fixed rates, the general downward trend in interest rates can also impact ARMs when they adjust. Even if you have an ARM now, keeping an eye on these fixed-rate shifts is wise, as they can signal a broader easing of borrowing costs.

What’s Driving These Rate Declines?

While Freddie Mac doesn't always detail the exact causes in their regular survey report, we can infer some common factors that influence mortgage rates. Generally, mortgage rates tend to follow trends in the broader bond market, particularly the yields on U.S. Treasury bonds. Economic indicators, inflation data, and the Federal Reserve's monetary policy play huge roles.

When inflation is seen as under control and the economy is stable, investors are often willing to accept lower returns on bonds, which can push mortgage rates down. Conversely, if inflation fears rise, bond yields (and thus mortgage rates) can climb. The fact that rates have declined over the past year suggests that factors like moderating inflation and a stable economic outlook have been at play. It's a delicate dance, and right now, it seems the music is playing a slower, more affordable tune.

Looking Ahead: What Could Happen Next?

Predicting interest rates with certainty is a fool's errand – even the experts get it wrong sometimes! However, based on this trend and general economic principles, here’s what I’m keeping an eye on:

- Federal Reserve Policy: The Fed’s decisions on interest rates are a massive influence. If they signal future rate cuts or maintain a dovish stance, it could help keep mortgage rates relatively low.

- Economic Growth: Strong economic growth can sometimes lead to higher inflation and, consequently, higher rates. A moderate growth rate is often best for stable, lower mortgage rates.

- Inflation: Continued progress in bringing inflation down will be a key factor in keeping rates from climbing again.

For now, though, the data points to a positive environment for borrowers. This stability around the 6.18% mark for the 30-year fixed is a rare and valuable opportunity.

The Bottom Line

As of December 24, 2025, the average 30-year fixed-rate mortgage stands at 6.18%, a welcome decrease of 67 basis points from a year ago. The 15-year fixed-rate mortgage is holding steady around 5.50%. This period of stable, lower rates provides a valuable window for individuals looking to purchase a home or refinance their existing mortgage. My professional opinion is that anyone considering a move or a refi should absolutely be exploring their options right now. Don't let this opportunity pass you by!

VS

Two solid options: Alabama’s affordable new build with steady returns vs Tennessee’s larger home with higher cash flow. Which fits YOUR investment strategy?

📈 Choose Your Winner & Contact Us Today!

Talk to a Norada investment counselor (No Obligation):

(800) 611-3060

Invest in Fully Managed Rentals for Smarter Wealth Building

With mortgage rates dipping to their lowest levels in months, savvy investors are seizing the opportunity to lock in financing.

By securing favorable terms now, you can also maximize immediate cash flow while positioning yourself for stronger long‑term returns.

Norada Real Estate helps you seize this rare opportunity with turnkey rental properties in strong markets—so you can build passive income while borrowing costs remain historically low.

🔥 HOT NEW LISTINGS JUST ADDED! 🔥

Talk to a Norada investment counselor today (No Obligation):

(800) 611-3060

Also Read:

- How Mortgage Rates Dropped From 7% Highs to 6.2% Lows in 2025

- Mortgage Rates Predictions Backed by 7 Leading Experts: 2025–2026

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?