Ever wondered how much house prices have changed in the US over the last two decades? The house price graph for the last 20 years in the USA tells a fascinating story, full of ups and downs. It's a story of booms and busts, of changing interest rates, and of the dreams of millions of Americans. Let's dive in!

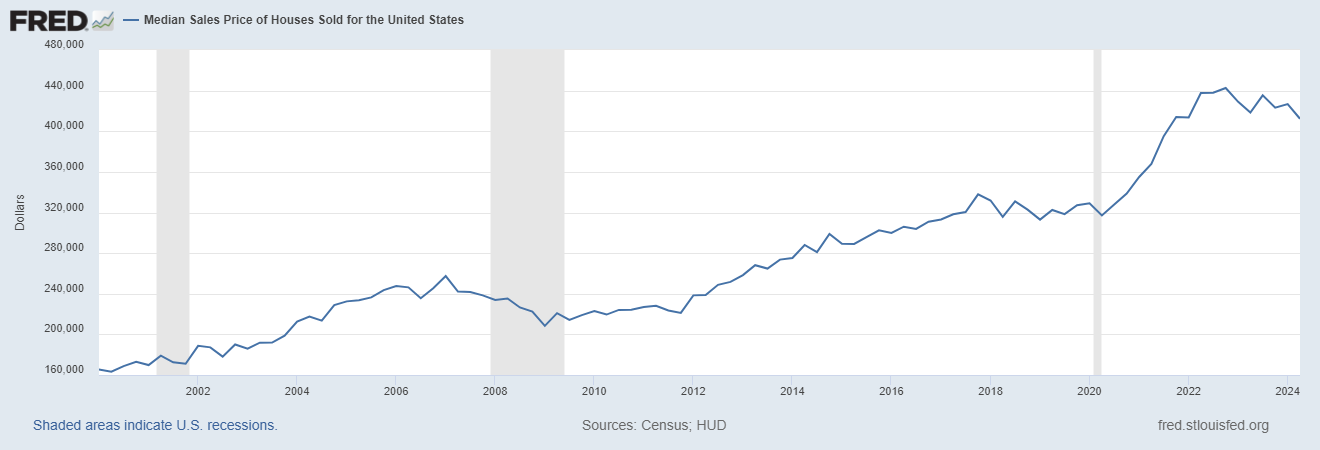

This data, reflecting the median sales price of houses sold, can be explored through resources like FRED (Federal Reserve Economic Data). Specifically, the U.S. Census Bureau and U.S. Department of Housing and Urban Development provide this valuable data, tracked as the Median Sales Price of Houses Sold for the United States.

House Price Graph Last 20 Years USA: A Rollercoaster Ride

The Early 2000s: A Steady Climb

- House Prices on the Rise (2000-2006): At the start of the millennium, the U.S. housing market experienced a period of significant growth. The house price graph for the last 20 years (including the years leading up to 2006) showed a steady upward trend. Back in 2000, the median price of a house hovered around $165,300. Over the next few years, prices kept climbing, reaching $247,700 by early 2006, an increase of roughly 50% in just six years. This rapid appreciation was fueled by a combination of factors, including low interest rates, relaxed lending standards, and a general belief that housing prices would continue to rise indefinitely. This optimistic outlook encouraged increased demand and speculation in the housing market. Things looked good, and many people felt confident about investing in real estate, often taking out mortgages they could barely afford in the expectation that rising home values would quickly build equity. This exuberance, however, would soon prove to be unsustainable.

The Housing Bubble Bursts (2007-2009)

- The Crash: Then, the music stopped. The housing bubble, fueled by risky subprime loans, adjustable-rate mortgages, and rampant speculation, burst with a deafening silence. The house price graph took a dramatic plunge, resembling a ski slope after an avalanche. By early 2009, the median price had plummeted to $208,400, erasing years of steady growth and leaving countless homeowners underwater. This wasn't just a dip in the market; it was a freefall. Families who had treated their homes as piggy banks, relying on ever-increasing values to refinance and access equity, suddenly found themselves trapped. Foreclosures skyrocketed, neighborhoods were dotted with abandoned properties, and the ripple effect spread through the economy. I remember talking to my neighbor, Mr. Johnson, back then. He was worried sick about his mortgage, facing the very real possibility of losing the home he'd worked his entire life for. His story wasn't unique. Everyone was feeling the pinch. Businesses closed, unemployment soared, and the nation teetered on the brink of a full-blown depression. The fear was palpable. You could feel it in the air, a heavy blanket of uncertainty draped over everything.

Recovery and Growth (2010-2019)

- Slow and Steady: The years following the crash were a period of slow but steady recovery. The USA house price graph started to climb again, although at a more moderate pace. This more sustainable growth was partly due to tighter lending regulations enacted after the crisis, making it more difficult for borrowers to obtain mortgages with risky terms. Things weren't booming like before, but they were getting better. By 2019, the median house price had climbed back up to over $327,100. It felt like we were finally turning a corner. This renewed sense of stability encouraged more buyers to enter the market, further fueling the recovery, albeit cautiously. Construction also began to pick up, slowly addressing the housing shortage that had developed during the downturn. However, lingering concerns about affordability remained, particularly in major metropolitan areas where prices were rising fastest.

The Pandemic and Beyond (2020-2024)

- Unexpected Surge: Then came the COVID-19 pandemic, and something unexpected happened. Low interest rates implemented to stimulate the flagging economy and a dramatic shift towards working from home fueled a huge, and arguably artificial, demand for houses. People suddenly needed more space for home offices, desired larger properties further from urban centers, and were incentivized by historically low borrowing costs. This confluence of factors created a fiercely competitive market, pushing prices to over $442,600 by late 2022. This rapid appreciation led to concerns about affordability and raised questions about the long-term sustainability of the market, especially given the potential for a housing bubble. Many were left wondering if this surge was a temporary anomaly driven by the unique circumstances of the pandemic or a fundamental shift in the housing market landscape.

- Recent Cooling: However, as interest rates started to rise again in 2023, the market began to cool off. As of Q4 2024, the median house price is around $426,800. This cooling trend is largely attributed to the Federal Reserve's efforts to combat inflation, making borrowing more expensive for potential homebuyers. The increased cost of mortgages has reduced affordability, pushing some buyers out of the market and putting downward pressure on prices. What will happen next? It's hard to say for sure. Several factors could influence the market's trajectory, including the pace of future interest rate hikes, the overall health of the economy, and the continuing inventory shortage. If interest rates stabilize or even decrease, we could see renewed buyer interest and potentially a rebound in prices. Conversely, a further economic slowdown or continued aggressive rate hikes could exacerbate the cooling trend and lead to more significant price declines. The housing market remains dynamic and sensitive to economic shifts, making it difficult to predict the future with certainty.

Table: Median House Prices (Quarterly Data)

| Year | Q1 | Q2 | Q3 | Q4 |

|---|---|---|---|---|

| 2020 | $329,000 | $317,100 | $327,900 | $338,600 |

| 2021 | $355,000 | $367,800 | $395,200 | $414,000 |

| 2022 | $413,500 | $437,700 | $438,000 | $442,600 |

| 2023 | $429,000 | $418,500 | $435,400 | $423,200 |

| 2024 | $426,800 | $412,300 | $415,300 | $414,500 |

What Drives these Changes?

Several factors influence US house prices over the last 20 years:

- Interest Rates: Lower interest rates make it easier for people to borrow money to buy houses, which pushes prices up. Higher rates do the opposite.

- The Economy: When the economy is doing well, people have more money to spend, and house prices tend to rise.

- Supply and Demand: If there are more buyers than sellers, prices go up. If there are more sellers than buyers, prices go down.

What's Next?

Predicting the future of the US house price graph is tough. No one has a crystal ball. However, by understanding the trends of the past and keeping an eye on the factors that influence the market, we can make more informed decisions about buying or selling a home.

My Take: I've been watching the housing market for years, and it's always interesting to see how things change. Right now, it seems like the market is taking a breather after the pandemic frenzy. It's important to remember that real estate is a long-term investment. Don't let short-term fluctuations scare you.

Related Articles:

- Housing Market Graph 50 Years: Showing Price Growth

- San Diego Housing Market Graph 50 Years: Analysis and Trends

- Average Housing Prices by Year in the United States

- Average Home Value Increase Per Year, 5 Years, 10 Years

- How Much Did Housing Prices Drop in 2008?

- Housing Market Crash 2008 Explained: Causes and Effects

- Housing Market Predictions for Next 5 Years: 2025 to 2029

- Housing Market Predictions for Next Year: Prices to Rise by 4.4%

- Housing Market Predictions for the Next 4 Years: 2024 to 2028