Great news for anyone dreaming of owning a home or looking to refinance: the average rate on a 30-year fixed mortgage has dropped by 34 basis points compared to this time last year. This means borrowing money for your home is getting a little cheaper, which is always a welcome change in the housing market.

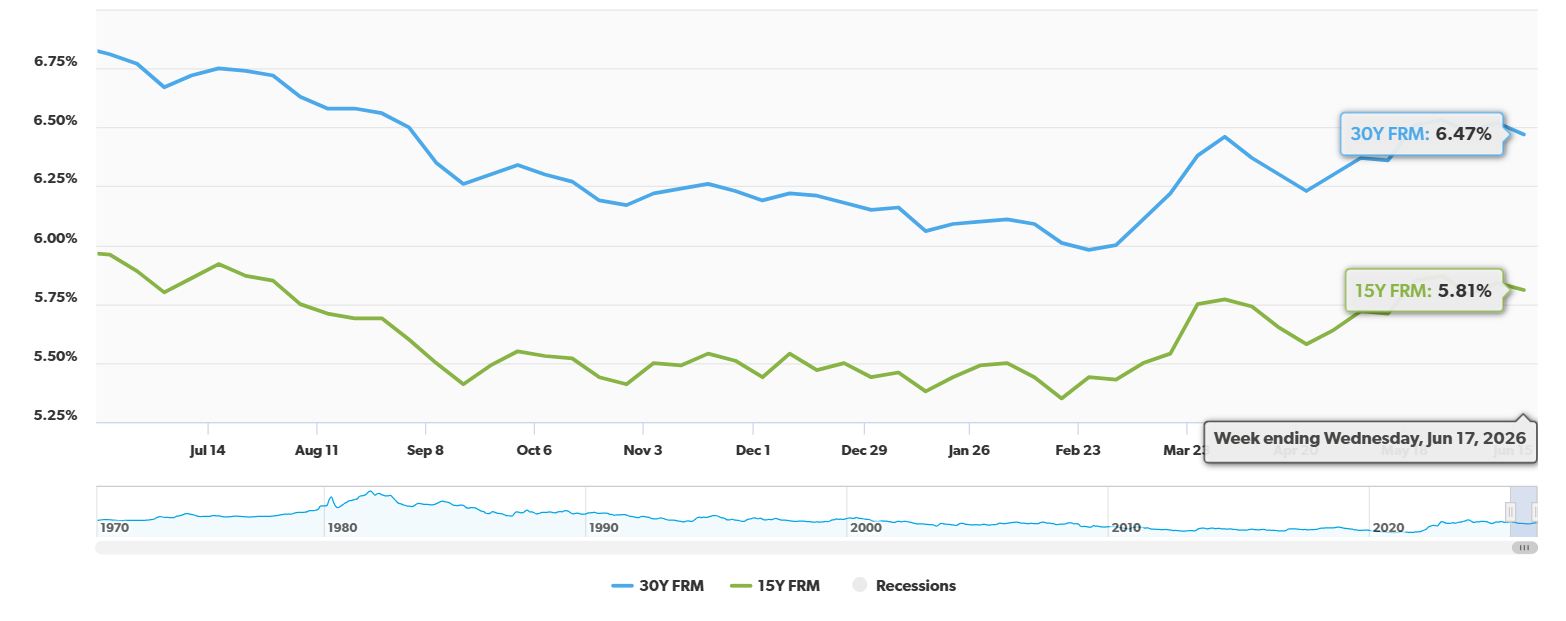

Even small changes in mortgage rates can make a big difference over the long run. Freddie Mac, a well-known source for housing data, recently shared that the average rate for a 30-year fixed mortgage is now 6.47%. That’s down from 6.81% a year ago. While it might not sound like a huge difference day-to-day, over the 30 years you'll be paying off your home, it can add up to serious savings.

30-Year Fixed Mortgage Rate Drops by 34 Basis Points From Last Year

What Does This Rate Drop Mean for You?

Let's break down what this means in plain English. A “basis point” is just a fancy way of saying one-hundredth of a percent. So, a 34 basis point drop means the rate is 0.34% lower.

On a $400,000 loan, this actually saves you a good chunk of money over time. Imagine this:

| Metric | Last Year (6.81%) | Today (6.47%) | Savings |

|---|---|---|---|

| Monthly Payment | $2,610.37 | $2,520.39 | ~$90 per month less |

| Lifetime Interest | $539,732.14 | $507,339.23 | ~$32,000 less overall |

See? That $32,000 in savings is money you won't have to pay back in interest. That’s huge! It’s like getting a nice bonus over the life of your loan.

Why Did the Rates Go Down?

Several things can influence mortgage rates, and this recent drop is likely due to a few factors working together.

1. Good News on the World Stage: One big reason rates often move is based on how folks feel about the global economy. Recently, there's been some positive news about peace talks in a conflict with Iran. When big global worries ease up, it often calms down the bond market, and that can lead to lower mortgage rates. Think of it like a storm passing – things feel safer, and that makes borrowing money cheaper.

2. What the Big Banks are Doing (or Not Doing): The Federal Reserve, which is like the country's main bank, has been keeping a close eye on prices. Even though mortgage rates went down this week, the Federal Reserve decided to keep its main interest rate steady. They're still a bit worried about prices going up too fast, so they might raise rates later. This tells lenders to be a little cautious, but the good news from abroad helped push mortgage rates down for now.

3. People are Still Buying Homes: Despite all the ups and downs, the housing market is showing it's strong. Things like people buying more stuff at stores and more people looking at homes (pending home sales) are good signs. This means there's still interest in buying houses, which helps keep things steady.

A Look at the Numbers: This Week vs. Last Year

Here’s a quick look at how rates have changed, thanks to Freddie Mac's survey:

| Mortgage Type | This Week (6.47%) | Last Week (6.52%) | Last Year (6.81%) |

|---|---|---|---|

| 30-Year Fixed Rate | 6.47% | 6.52% | 6.81% |

| 15-Year Fixed Rate | 5.81% | 5.84% | 5.96% |

As you can see, both the 30-year and 15-year fixed rates are lower than they were last year. The 15-year fixed rate, which is a shorter loan term, is also lower than it was just last week.

Does This Mean I Should Buy or Refinance Right Now?

That’s the million-dollar question, isn't it? This drop is definitely a positive sign. The $32,000 savings over the life of a loan is significant. It could mean you can afford a slightly bigger house for the same monthly payment, or it could simply mean you pay off your mortgage faster with fewer interest costs.

However, it’s also important to be realistic. While saving $90 a month feels good, it might not feel like a huge change when you look at your overall budget, especially if home prices are still high where you live.

Also, remember that mortgage rates have been much lower in the past. We saw rates in the 3% to 4% range for many years. So, while today's rates are better than last year, they're still higher than that recent historical low.

When you're thinking about buying a new home or refinancing your current one, you have to consider the costs involved, like closing costs. These fees can add up, and it might take a few years of those $90 monthly savings to cover those upfront expenses.

My Two Cents: Keep an Eye on the Market

As a homeowner myself and someone who follows this stuff closely, my advice is to always do your homework. This rate drop is fantastic news, and it definitely makes things more affordable. It's a good time to:

- See if you qualify for a lower rate: If you're thinking about refinancing, now might be the time to talk to a lender and see what kind of rates you can get.

- Explore buying a home: For those looking to buy, lower rates mean a more manageable monthly payment.

- Understand your options: Don't just jump into anything. Compare offers from different lenders and make sure the numbers make sense for your personal situation.

The housing market is always moving, and these rate changes are part of that rhythm. Enjoy the good news, but stay informed!

VS

Out‑of‑State investors can compare Tennessee’s newer rental with higher NOI vs Florida’s A+ property with strong yield. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain near 6%, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- Will Mortgage Rates Drop to 5% in 2026: Expert Forecast

- How to Get a 3% Mortgage Rate in 2026 With Assumable Mortgages?

- How to Get a 4% Interest Rate on a Mortgage in 2026?

- What Leading Housing Experts Predict for Mortgage Rates in 2026

- Mortgage Rate Predictions for 2026: What Leading Forecasters Expect

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?