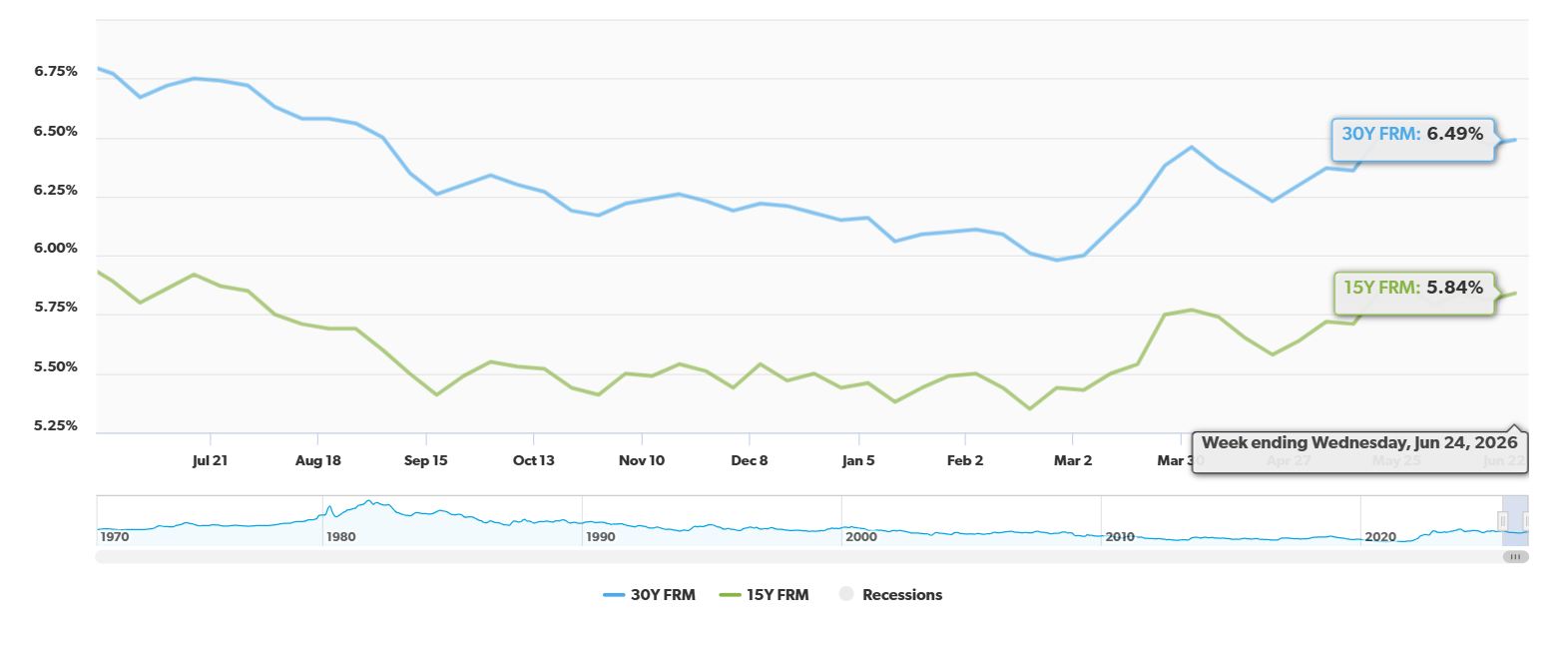

The average 30-year fixed mortgage rate has dipped by 28 basis points compared to this time last year, now sitting at 6.49%. While this might sound like a small shift, it could be the breathing room some potential homeowners and refinancers have been waiting for.

I've been following the mortgage market for a while now, and these kinds of shifts, even if they seem minor on the surface, can have real ripple effects. It’s easy to get lost in the numbers, but what does this particular drop really signal for anyone thinking about buying a home or restructuring their current mortgage? From my perspective, it's a mixed bag, offering some relief but also highlighting the persistent economic forces at play.

30-Year Fixed Mortgage Rate is Down by 28 Basis Points Year Over Year

A Closer Look at the Numbers: Freddie Mac's Latest Survey

The data we're talking about comes straight from Freddie Mac's Primary Mortgage Market Survey (PMMS), a respected source for mortgage rate trends across the U.S. They recently reported that the average rate for a 30-year fixed mortgage has settled at 6.49%. This is a noticeable step down from the 6.77% we saw exactly one year ago.

However, it’s not all smooth sailing. If you look at the last week, the rate actually ticked up by a small margin – 2 basis points – from 6.47% to 6.49%. This stagnation over the past six weeks, hovering stubbornly around the 6.5% mark, tells its own story, largely driven by persistent inflation worries and what people are expecting from the Federal Reserve.

To give you a clearer picture, let's break down how this year-over-year change looks for different loan types:

| Loan Type | Current Weekly Average | Rate One Year Ago | Year-Over-Year Change |

|---|---|---|---|

| 30-Year Fixed | 6.49% | 6.77% | -0.28% (-28 bps) |

| 15-Year Fixed | 5.84% | 5.89% | -0.05% (-5 bps) |

As you can see, the 30-year fixed has seen the most significant year-over-year drop among these popular options.

What’s Really Moving the Market? My Take on the Driving Forces

So, why aren't rates just plummeting, even with this year-over-year improvement? From what I’m observing, a few key factors are keeping things in check:

- Stubborn Inflation: This is the big one. Recent economic reports suggest that inflation isn't cooling off as quickly as we'd hoped. This makes the bond market nervous. When inflation is high, the value of future returns decreases, so investors demand higher yields on bonds. This “higher-for-longer” interest rate expectation is definitely capping any drastic drops in mortgage rates. I've seen this play out before – if inflation is sticky, the Fed tends to keep interest rates elevated to try and bring it under control, and mortgage rates follow suit.

- Treasury Yields as a Compass: Mortgage rates don't exist in a vacuum. They tend to move in close step with the yields on the 10-year U.S. Treasury note. Right now, the 10-year Treasury yield has been hovering around the 4.4% range. This alignment means that as long as Treasury yields stay relatively stable or only dip slightly, mortgage rates will likely mirror that behavior, preventing any dramatic freefalls.

- Shifting Borrower Needs: It's interesting to see how people are reacting. While the overall pace of home purchases has slowed a bit (which is understandable when rates are higher than many hoped), Freddie Mac is noticing an uptick in refinancing activity. This makes sense! If you bought a home when rates were higher, or if you're looking to tap into home equity, even a modest drop like this can translate into significant savings on your monthly payments. It's a smart move for those who can benefit.

Navigating the Current Rate Environment: What I Recommend

Given this situation, where rates are down year-over-year but a bit stagnant week-to-week, here are some actionable steps I'd suggest:

- Lock Your Rate: If you're deep in the home-buying process and have an accepted offer, don't wait. Mortgage rates can swing by a quarter of a percent or more in a single day. Talk to your lender today about getting a rate lock. This secures a specific rate for you for a set period, protecting you from any upward movement while you finalize your purchase. I always tell my clients to be proactive here.

- Keep an Eye on the Refinance Window: If you purchased your home within the last couple of years, especially when rates were closer to their peak (think 7% or even 8%), a rate around 6.49% might be a golden opportunity to refinance. Even a half-percentage-point drop can save you hundreds of dollars per month over the life of your loan. Do the math – it might be worth it.

- Shop Around and Compare: This is crucial and something many people overlook. Lenders don't all offer the same rates or fees. Even a small difference in the advertised rate can add up to thousands of dollars over 30 years. I strongly advise getting quotes from at least three to four different lenders. Use online tools like NerdWallet or Bankrate to get a sense of daily averages, but always have direct conversations with lenders.

The Bottom Line: A Modest Improvement, But Context is Key

So, what does this all add up to? The fact that the 30-year fixed mortgage rate is down 28 basis points year-over-year is good news, plain and simple. It signals a more favorable environment than we had a year ago. However, the recent week-over-week uptick and the overall stability around 6.5% remind us that we're still in a market shaped by economic uncertainties, particularly inflation.

For buyers, this drop might make homeownership slightly more accessible than it was last year, potentially lowering monthly payments. For those considering refinancing, it’s definitely a window worth watching. It’s not a dramatic crash that would send rates to historic lows, but it’s a tangible improvement that can make a difference. My advice? Stay informed, be prepared to act quickly when the opportunity arises, and always do your homework.

VS

Out‑of‑State investors can compare Tennessee’s newer rental with higher NOI vs Florida’s A+ property with strong yield. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain near 6%, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- Will Mortgage Rates Drop to 5% in 2026: Expert Forecast

- How to Get a 3% Mortgage Rate in 2026 With Assumable Mortgages?

- How to Get a 4% Interest Rate on a Mortgage in 2026?

- What Leading Housing Experts Predict for Mortgage Rates in 2026

- Mortgage Rate Predictions for 2026: What Leading Forecasters Expect

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?